If you’ve been trading on Polymarket over the past 24 hours and something about fees felt… off, you weren’t imagining it.

The prediction market platform rolled out a comprehensive fee structure on March 30, expanding taker fees across most categories and moving away from what had largely been a free-to-trade environment. That alone is a meaningful shift.

But what’s more interesting is what happened immediately after. Within a day on March 31st, Polymarket adjusted the system again. Not because the idea was wrong, but because part of the implementation was.

Polymarket only launched in 2020, but has quickly become one of the largest and most popular prediction market platforms in the world.

In the new model, fees scale with uncertainty, and takers pay for the convenience of executing immediately against the order book. When a market is around 50%, fees are highest. As outcomes move toward 0% or 100%, fees drop off. Unfortunately, early on, users began to notice something strange. In certain markets, especially weather and economics, trades at very low prices were getting hit with unexpectedly high fees. Screenshots circulated, and the reaction was pretty immediate.

According to the Polymarket team, the issue wasn’t the curve itself, but how fees were being calculated. Originally, they were tied to USD taker volume, which created distortions at the tails. In low-price markets, this made fees look much larger than intended relative to the actual position.

Polymarket has now fixed this by switching to a share-based calculation, which is more in line with how exchanges typically operate. Now that we understand what changed and what’s already been fixed, it’s worth stepping back and asking a more important question: why structure fees this way at all, and why do different types of trades get charged differently?

As someone who tends to trade in high-confidence markets, usually above 90¢, this was especially frustrating. Under the old model, if you put $100 into a 95¢ contract, the fee was tied to the full $100 trade value even though the profit on that position was only around $5.

That’s what made the structure feel out of sync with the trade's actual economics. The move to share-based fees is a much cleaner approach because it aligns fees with position size instead of price, so in high-probability markets, you’re not paying disproportionately high fees relative to the small remaining upside.

There are two types of traders in this world: makers and takers. If you’re less familiar with that distinction, it’s worth understanding because it now directly affects how much you pay.

A taker is someone who wants to trade immediately. You hit “buy” or “sell,” and your order executes against whatever is already available in the market. A maker is someone who places a limit order and waits. You’re effectively saying, “I’m willing to buy at this price” or “sell at this price,” and letting someone else come to you.

Takers consume liquidity. They remove available orders and push prices around. Makers provide liquidity. They sit in the book, making it easier for everyone else to trade.

Because of this:

Takers now pay fees (roughly ~0.75% up to ~1.8%)

Makers continue to pay nothing and can even earn 20–25% rebates

The reasoning is pretty straightforward. If everyone acted like a taker, markets would be thin, jumpy, and expensive to trade. There wouldn’t be enough resting orders, spreads would widen, and prices would move too easily. So exchanges incentivize the opposite behavior. They charge for immediacy and reward patience.

Why Takers Get Charged More in Toss-up Markets

Taker fees peak around markets trading at around 50/50 because that’s where:

Uncertainty is highest

Disagreement is strongest

Trades are most likely to be informed

If you’re trading at 50%, you’re not just clicking buttons. You’re expressing a view in the most competitive part of the market, often reacting to new information. From the platform’s perspective, that’s the most “valuable” part of the system, and the most costly to maintain in terms of liquidity. So fees are highest there. At the edges, 90%, 95%, 5%, there’s less disagreement, less active trading, and less need to tightly manage liquidity. So fees fall off.

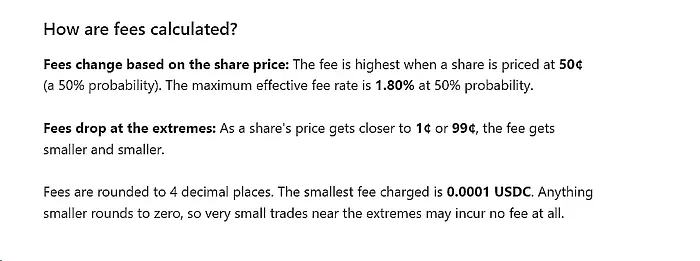

Polymarket's explanation of fees:

What This Means in Practice

The main shift isn’t just that fees exist. It’s that your trading style now matters more.

If you:

Trade frequently

Chase moves around breaking news

...or operate in that 40–60% range

...you’re now paying for that immediacy in a much more explicit way.

If instead you:

Place limit orders

Sit on positions

...or trade at the tails

...your costs are lower, and in some cases, you’re actually being subsidized. That’s a pretty meaningful change in incentives, even if it doesn’t look dramatic at first glance.

Bottom Line - What do Polymarket's New Fees Mean to Traders?

If you’re trading on Polymarket, the takeaway is pretty simple.

Fees are now part of the equation, especially in the middle of the market. The earlier issues that made some trades unusually expensive have mostly been fixed, but the broader shift toward a more structured system is here to stay.

Prediction markets involve risk and are not suitable for everyone. While many platforms offer tools to make informed trades, outcomes are never guaranteed, and users should never risk more than they can afford to lose. Always trade responsibly. Additionally, platform availability and legal status vary by region. It is your responsibility to check local laws and verify that you are legally allowed to use a given platform before participating.

While the rollout clearly caused a wave of frustration, especially on Twitter, I think the bigger takeaway is how quickly Polymarket responded. The team moved fast to overhaul the structure and correct unintended issues, which should give users some confidence.

In a space this new, it’s less about getting everything perfect on day one and more about how quickly platforms adapt when something doesn’t work.

button in Safari

button in Safari